Last Updated on Jun 27, 2023 by Anjali Chourasiya

There are a handful of stocks that have earned a ‘never bet against’ status in the Indian markets. And Avenue Supermarts, better known as DMart, has definitely been part of that elite clan.

Usually, the reason for a stock achieving this stature is pretty simple – make money for investors. With an issue price of Rs. 299, and a blockbuster listing at Rs. 600 in March 2017, DMart reached an all-time high of Rs. 5,899 in October 2021. That’s almost 10x in less than 5 years.

Also responsible for gaining immense faith among investors was the pedigree of its founder Radhakishan Damani, who has been a celebrity investor through the 1990s. He’s known for having made some serious money in the stock markets and has a portfolio that is closely tracked by the market paps.

But whether you are an investor or not, what has been unnoticeable in the case of DMart is its popularity; from a consumer’s POV. Full parking spaces, rubbing shoulders with other shoppers in tiny aisles, and getting daunted by long queues may be a dampening shopping experience, but when so many people hustle to buy something, you know there’s something special about it.

And despite the shoppers’ year-round frenzy, the stock is down more than 40% in just a year and a half, leaving the fandom worried. So, what’s the sudden anticlimax about?

Table of Contents

What’s wrong with DMart?

On the face of it, it looks like nothing is wrong with DMart. In FY 2023, its revenue grew by 38% y-o-y, and PAT grew by 59%. But a deeper dig into the numbers highlights enough reasons to explain why the stock has been such an under-performer.

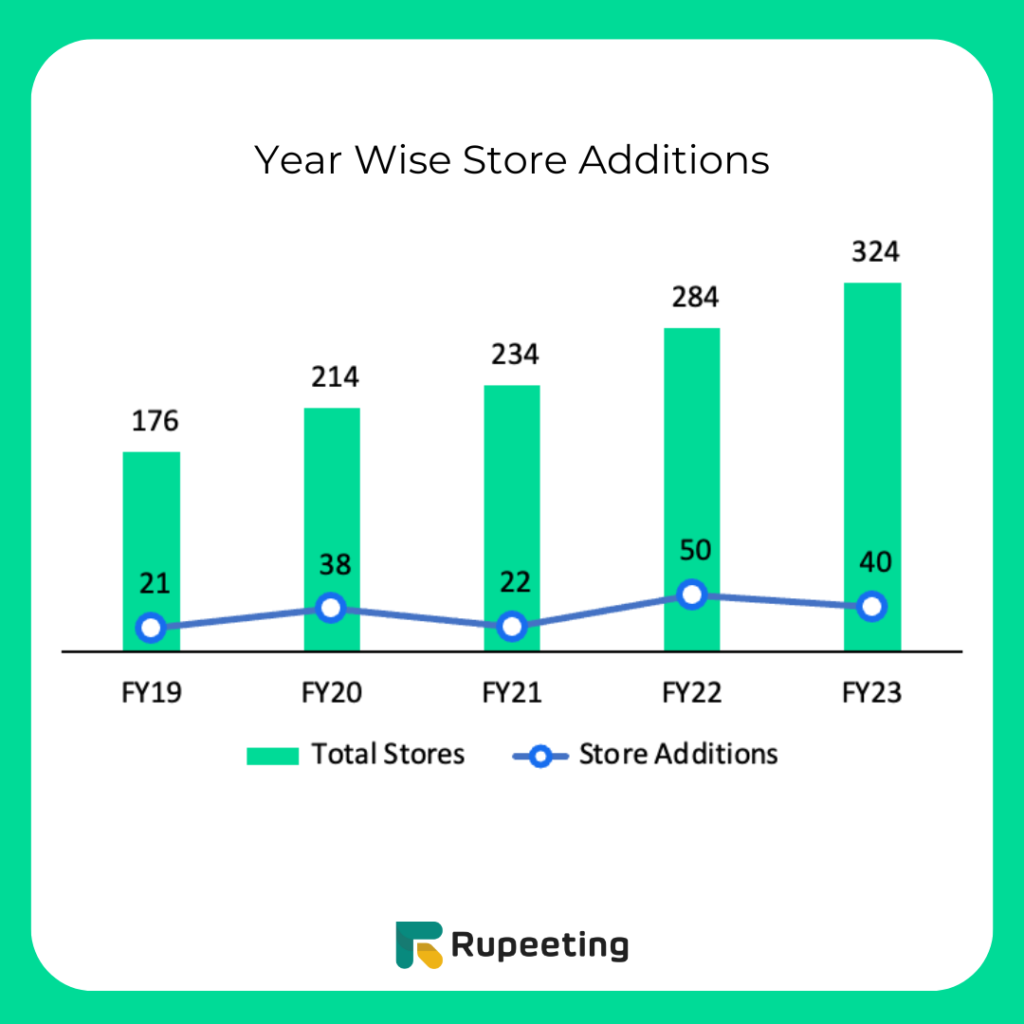

1. Store additions

In retail, the simplest form of gauging growth is by seeing how many stores are being added. And on this front, there has been a question raised on DMart’s prowess.

Naturally, the pandemic affected the offline retail business dramatically. In FY 2020 DMart had added 40 stores, and that almost halved to just 22 stores in FY 2021. From there, it did make a bit of a recovery with 50 new stores in FY 2022. But with the number dropping again to 40 additions in FY 2023, the recovery in store additions has been looked at as patchy.

But what’s got investors sweating is the fact that compared to Reliance Retail, these numbers look nothing but petty. While DMart had a total of 324 stores as of March 2023, Reliance Retail was at a mammoth 3,300. And it’s not just about how many more stores Reliance has, but about how fast it’s growing. In the March 2023 quarter, Reliance Retail added 966 stores, which is almost 3x of the total stores that DMart has.

Competition growing bigger and faster has been leading to a natural worry that DMart’s growth factors will start getting affected.

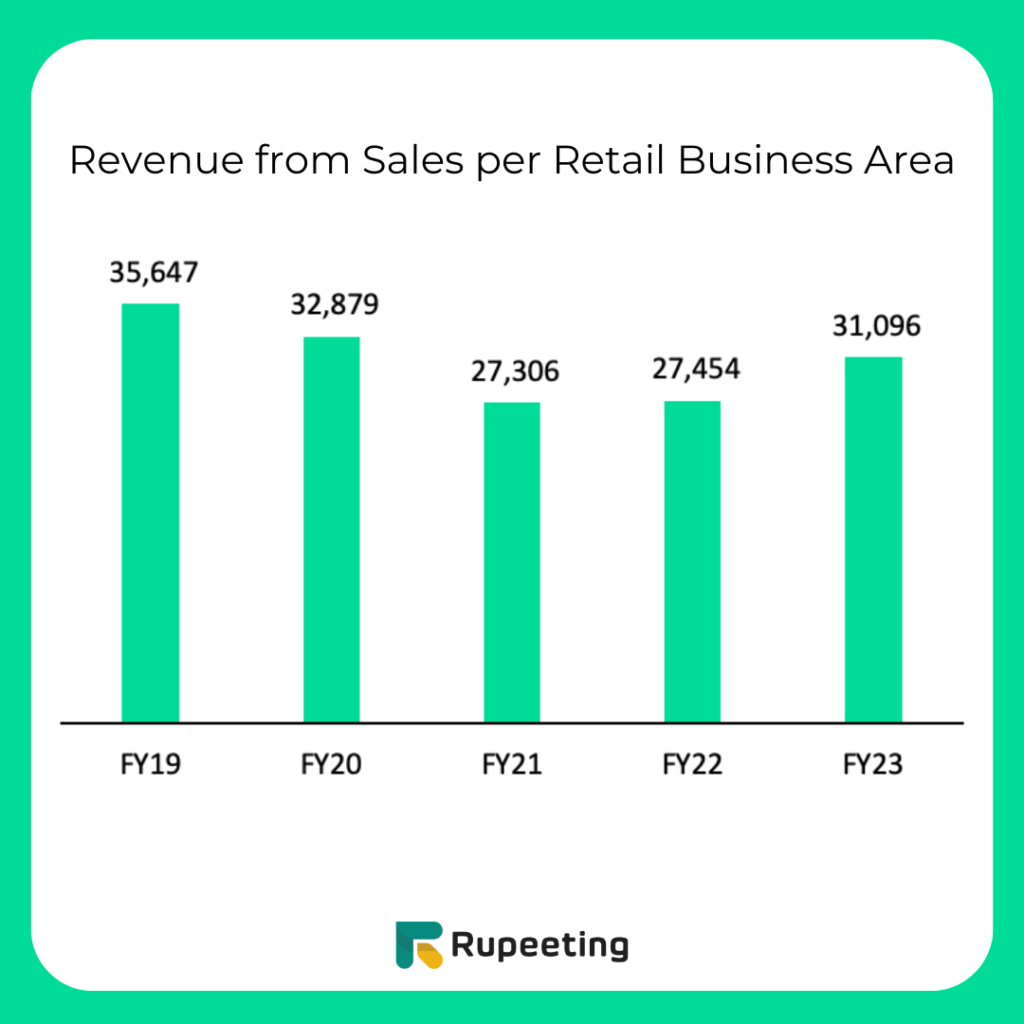

2. Revenue per square foot

Revenue per square foot adds context to store additions. After all, what’s the point of adding more stores if you can’t add more revenue per store?

Pre-pandemic, in FY 2019, DMart had a revenue per square foot of Rs. 34,647, which declined to Rs. 27,545 in FY 2022. Here are a couple of reasons for that:

DMart is a value retailer. Its target market is extremely price-conscious. And for this price-sensitive user, inflation has hit hard, causing household budget cuts and even price cuts by retailers in order to keep sales going.

Additionally, there has been a change in strategy for DMart, with it focusing on increasing the size of its stores. Earlier DMart stores were between 35,000- 40,000 square feet. However, as of now, of the 324 stores, around 60% are more than 45,000-50,000 square feet in size.

These two factors resulted in a drop in the revenue per square foot, which implies a deterioration in the quality of growth.

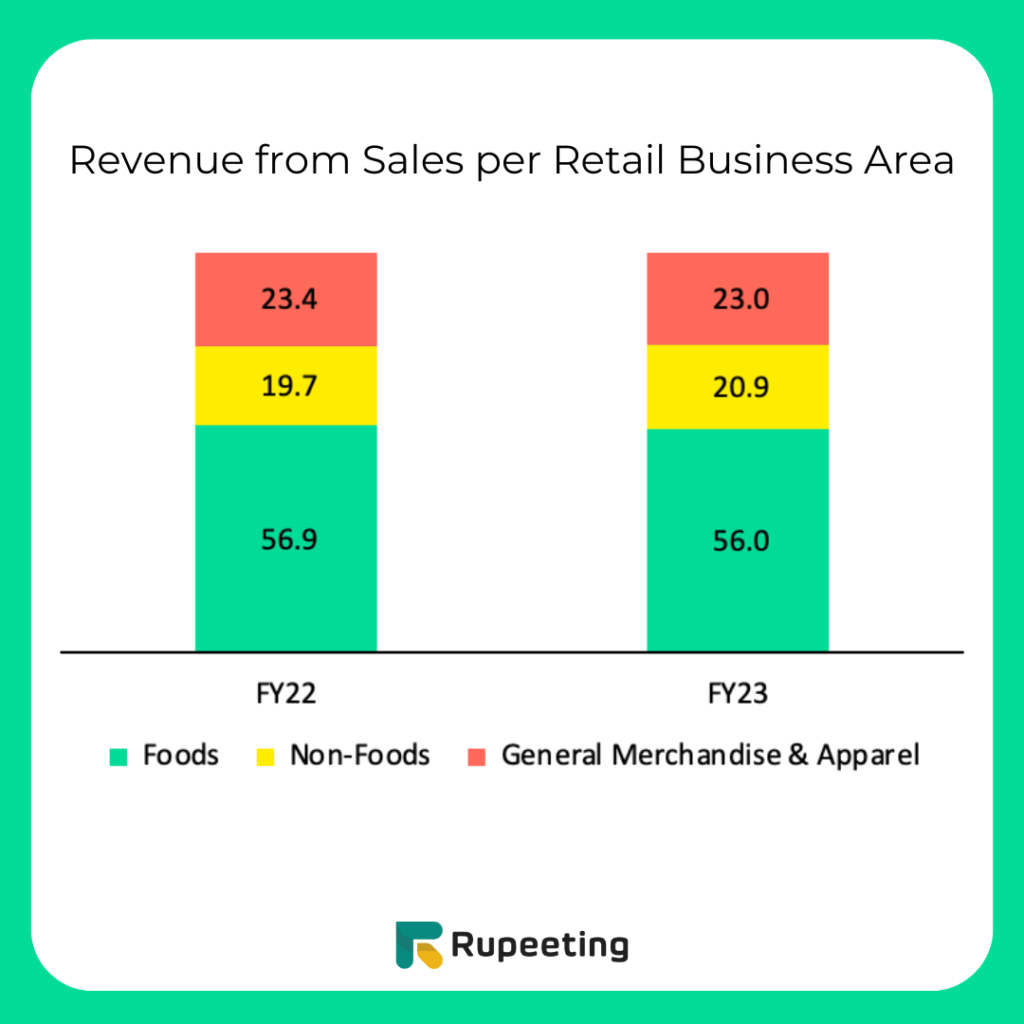

3. Revenue mix

DMart has three segments – Food, Non-Food, and General Merchandise & Apparel. Of these three, General Merchandise & Apparel has the highest margin, at 25-28%; whereas, Groceries fetch the lowest margin at 10-12%.

Lately, the higher margin segment of General Merchandise & Apparel has been seeing slower growth for DMart, thanks to the inflation-affected consumer and stiff competition.

Competition has been intensifying in the price segment that DMart caters to, with players like Zudio, Max and Reliance Retail not just growing larger but also offering lower prices and better customer experience.

The change in revenue mix, away from General Merchandise & Apparel, has been reflected in DMart’s margins.

DMart’s dismal profitability

The above factors have taken a toll on revenue growth and, more importantly, on profitability for DMart.

In Q4 FY 2023, while revenue growth was at 20% y-o-y, EBITDA growth came in at a mere 5%. To add some context, that 5% has been the slowest EBITDA growth since listing and was even lower than street expectations, which already seemed conservative.

In Q4 FY 2023, EBITDA margins were at 7.3%, compared to 8.4% a year ago. In addition to this, EBITDA per store was at Rs. 2.5 cr, versus Rs. 2.7 cr. a year ago. Gross margin compression, lower revenue per square foot because of increased store size, and a changing revenue mix have all resulted in dismal profitability.

So while the overall FY 2023 numbers look good, quarterly earnings and the underlying trends don’t seem too bright at this point.

The silver lining

Wait, wait, not all is bad at DMart!

There is an important metric in retail called the Same Store Sales Growth, or SSSG. It is a metric that measures the growth in revenue from store locations that have been in operation for at least one year. This is an important metric since it helps gauge the organic growth from existing stores and cuts out the impact of new stores.

For DMart, the same stores amounted to 72% of the network in the second half of FY 2023 and grew by 11%. The strong growth indicates that old stores are showing healthy growth and that the problem is, in fact, in new additions.

Now why are we calling this a silver lining? Remember how DMart is adding new stores that are larger? The fundamental reality of any business is that setting up requires an initial investment, which fructifies and pays off over time.

Improvement Underway

While DMart is adding newer and larger stores, it is bound to see a dip in unit financials and in profitability in the beginning. As footfall increases, more shelves get full, and higher conversion takes place, metrics for new stores are likely to see normalisation over time.

This is likely to lead to better revenue per square foot, higher EBITDA per store, and better performance on overall revenue growth, margins and even return ratios.

Take revenue per square foot, for example. It dropped from Rs. 34,647 in FY 2019 to Rs. 27,545 in FY 2022. However, in FY 2023, it inched up and rose to Rs. 31,096. To reach pre-pandemic levels, it could take a few quarters.

Additionally, easing inflation is a big sign of respite for DMart. Given its price-sensitive consumer base, any fall in inflation is expected to result in the following:

- Higher spending by consumers

- Better ability for DMart to price its products and not be pressured by offers and discounts to keep sales going

- Consumers looking beyond the absolutely necessary and increasing discretionary spending on the high-margin General Merchandise & Apparel segment

With these factors, it is expected that challenges would be short-lived in nature, and improvement will start reflecting in financial performance towards the end of 2023.

Never bet against DMart?

Despite the near-term hiccups and heightened competition, there is a lot that makes DMart a strong long-term business in a difficult industry.

- DMart owns its stores and doesn’t lease them, giving it the advantage of lower recurring costs, higher margins, and even the ability to weather challenging macroeconomic conditions.

- It has minimal debt on its books, making it a strong cash flow business without leverage.

- It has been prudent on store additions, balancing the focus on profitability instead of rampant expansion.

- Its focus on turning inventory helps it generate higher revenue, profits and returns on each of its stores.

But while the business is good, a stock being good or bad depends on what price you’re getting it at. And so far, thanks to its performance and fan following, it has traded at expensive valuations. While stocks with a long-term growth story and strong fundamentals are worth not letting go of, high valuations make it difficult to have a ‘buy at any price’ attitude.

However, the 40% fall has given the stock breathing space and cleared some of the froth on valuations, giving investors an opportunity to accumulate a robust long-term story whenever the hero takes a beating. After all, the protagonist does come out of a fight to win!

This article was authored by Prasanna Bidkar of Rupeeting. Check out Rupeeting’s smallcase.

The views and opinions stated in the content belong to the author. Rupeeting: Alphaware Advisory Services Private Limited does not uphold nor promote any of the views / opinions. | Rupeeting: Alphaware Advisory Services Private Limited is a SEBI registered market analyst (Regn. No. INA000015747)

- DMart – Will the Poster Boy Get Its Glam Back? - Jun 23, 2023