Last Updated on Sep 7, 2023 by Harshit Singh

A financial emergency or a cash crunch situation can make you look for funding options like loans or other alternatives. Availing a loan against a fixed deposit (FD) rather than a personal loan is better because the loan amount of up to 90% of your FD amount can be availed, whereas, you can only avail up to Rs. 35 lakh from a personal loan. Moreover, the exciting interest rates make it more appealing to draw a loan against a fixed deposit. Apart from this, the loan tenure of a fixed deposit is till the FD matures, rather than a personal loan, which is only up to 5 yrs.

So, instead of breaking your fixed deposit prematurely, get a loan against a fixed deposit. Without further ado, let’s dive into the details of the process, loan limit, interest rates, advantages and disadvantages of availing this loan.

Table of Contents

How does loan against fixed deposit work?

A loan against a fixed deposit works the same way as any other loan, where the borrower receives funds in a lump sum and repays in equal monthly instalments (EMI). It is a type of secured loan in which borrowers can avail funds by pledging their fixed deposit as collateral. This is where the Loan-to-Value (LTV) comes into play, which allows you to calculate the percentage of money you will get against your investment, i.e. fixed deposit. Usually for fixed deposits, the LTV can be anywhere between 90% and 95% of the deposit amount.

When banks provide a loan against fixed deposits, they generally charge roughly about 2% points more than the FD rate. For example, if the interest rate on your fixed deposit is 7%, the interest on loan against a fixed deposit would be 9%.

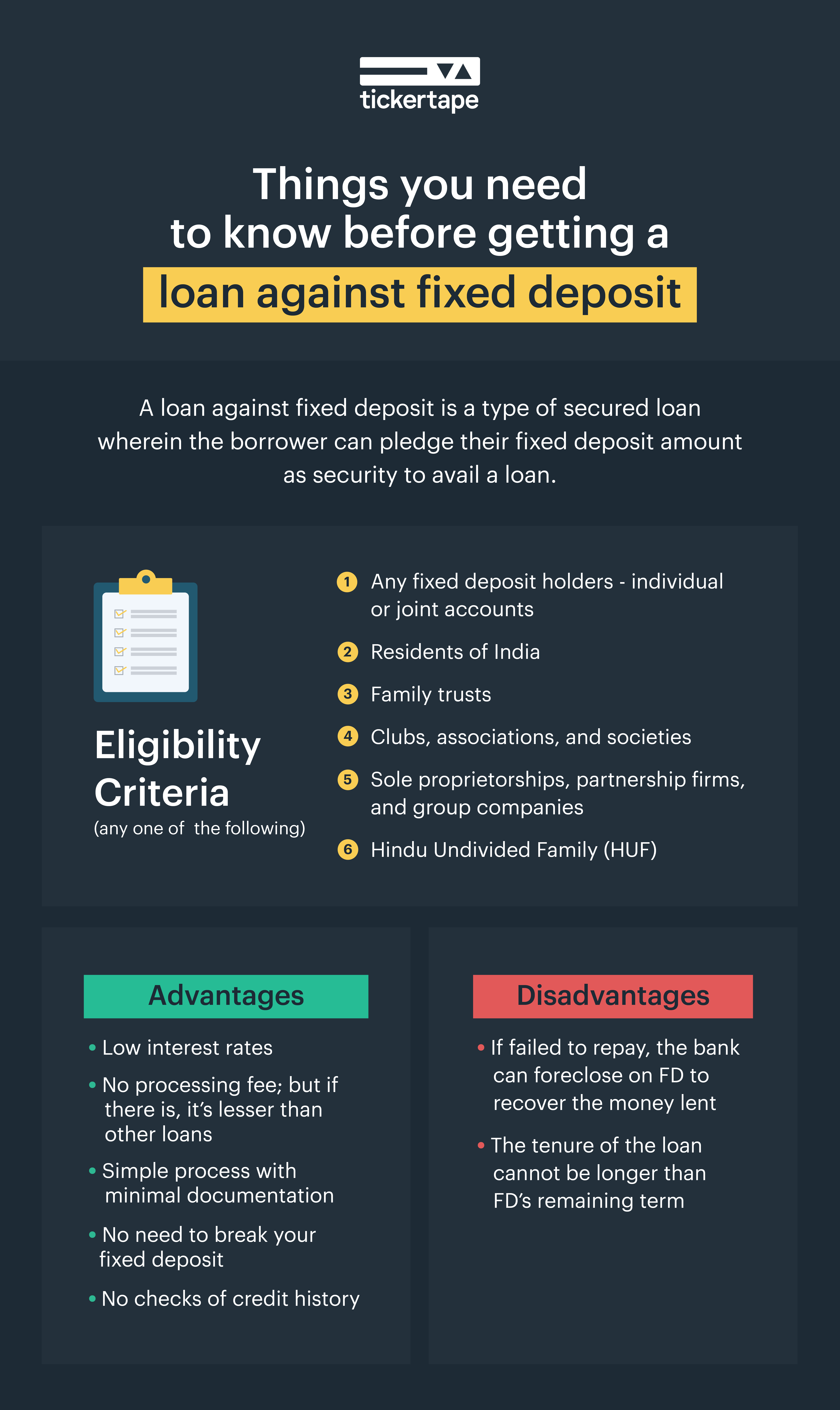

Eligibility criteria

The following is the criteria to be met in order to apply for a loan against FD:

- Can be availed by all fixed deposit holders, whether they are individual holders or have joint accounts.

- Resident citizens of India.

- Family trusts.

- Clubs, associations, and societies.

- Sole proprietorships, partnership firms, and group companies.

- Hindu Undivided Family (HUF).

Loan limit in banks

The below-mentioned table has the details of the loan limit in some of the major banks along with the interest rate:

| Banks | Loan Limit | Interest Rate |

| SBI | Up to 90% | FD Rate + 1% |

| HDFC Bank | Minimum Rs. 25,000 | FD Rate + 2% |

| Bank of Baroda | Up to 95% | FD Rate + 1% |

| ICICI Bank | Up to 90% | FD Rate + 2-3% |

| Citibank | Up to 90% | FD Rate + 1-2% |

| PNB | Up to 90% | FD Rate + 1% |

| Axis Bank | Up to 85% | FD Rate + 2% |

Source: My Loan Care

Advantages of a loan against fixed deposit

- A loan secured against fixed deposits carries a lower interest rate than other loan forms like personal loans.

- For a loan secured by an FD, most banks do not impose any processing fee. If the banks do impose a cost, it will be less than the processing fee for other types of loans.

- Loans against fixed deposits are processed quickly and require minimal documentation.

- The lender does not check your credit history. Fixed deposit serves as a security, which means that even if you default, the bank will recover the amount from your fixed deposit.

Disadvantages of a loan against fixed deposit

- On the flipside, if a borrower fails to repay the loan, the bank can foreclose on the fixed deposit to recoup the money lent.

- The tenure of the loan taken out against the FD cannot be longer than the fixed deposit’s remaining term.

On a side note: If you don’t have a fixed deposit and are in need of funds on an urgent basis, a personal loan could be the best alternative, depending upon the circumstance. In case you have a low credit score and are wondering whether or not your personal loan application gets approved, read How To Get a Personal Loan With a Low Credit Score to get a better understanding.

Overdraft facility on fixed deposit

Customers can get a loan against their FD as an overdraft from the banks. An overdraft is a financial instrument, which acts as an extension of credit when your savings or current account balance hits a zero. The fixed deposit-backed overdraft or OD limit is less than the deposit amount. The interest rate is only applied to the amount that is borrowed as an overdraft, and not to the entire limit.

For instance, if you have a fixed deposit of Rs. 10 lakh, a bank may authorize an OD of up to Rs. 9 lakh. The borrower has the option of withdrawing any amount up to Rs. 9 lakh. An overdraft does not have a set repayment period. The borrower is responsible for paying interest for as long as they hold the money.

When the amount required is less than the funds parked in the FD, taking a loan against it is preferable than liquidating it. For example, let’s say you have an FD of Rs. 10 lakh but only require Rs. 3-4 lakh, one way of meeting the funding need is by taking out a loan. The withdrawal of FD is subject to a penalty if done prematurely. In many circumstances, taking out a loan would be more cost-effective than paying the fine, particularly if the borrower has the ability to prepay it. And the prepayment can have charges applied so make sure to check them out.

One thing to keep in mind is that defaulting on a loan availed against a fixed deposit will impact your credit score.

- Top Fund of Funds (FOF) in India – Full Form, Types & More - Mar 28, 2025

- Bond Funds – Meaning, Types, Risks, and Benefits - Mar 27, 2025

- Money Market Mutual Funds: Meaning, Benefits, Liquidity and Taxation - Mar 13, 2025