– A Smart Alternative to Gold Exposure")

Last Updated on Jul 12, 2024 by Anjali Chourasiya

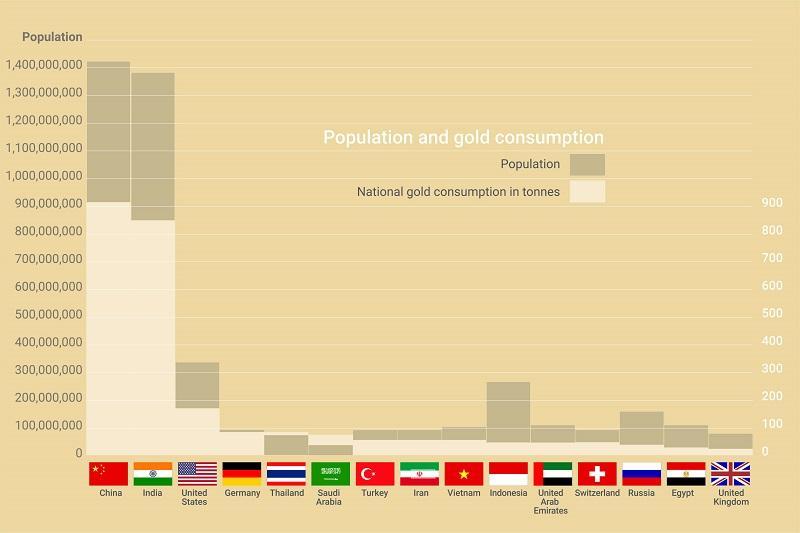

Since ancient times, gold has held deep emotional significance for Indians. In the past, whenever a family sold their ancestral gold, it was perceived as a sign of severe financial distress, a desperate last resort. Many Indian families and communities have a tradition of regularly buying gold, either annually or semiannually, for their children and presenting it to them at the time of their marriage. India has consistently ranked among the top three consumers and top five importers of gold.

However, importing gold primarily for consumption contributes to the growing fiscal deficit, creating economic challenges. To address these issues, the government launched the Sovereign Gold Bond (SGB) scheme in 2015. This scheme aimed to reduce the reliance on physical gold and decrease the fiscal deficit, thereby promoting the financial stability of the country.

Table of Contents

What exactly is the SGB scheme?

- SGB is a government backed investment alternative. SGB’s are issued by the RBI on the behalf of the Govt of India.

- The bonds are issued in multiple grams with a basic unit of 1 gram. There are maximum limitations to the SGB’s which is 4 kg for individuals and about 20kg for institutions.

- The bonds usually have a tenure of 8 years with an exit option after the 5th year.

Why should I invest my money in SGB’s and not in Physical gold?

Interest Income

SGBs offer an annual interest income of 2.5%, paid semiannually. This kind of incentive isn’t provided with physical gold.

Purity checks

The value of gold depends on its purity, making accurate quality assessment crucial for determining its worth. While 24 karat is the purest form of gold, it can sometimes be mixed with impurities that are not visible to the naked eye, potentially deceiving individuals. In SGB’s the purity is confirmed and backed by the government.

(Recently, a friend of mine bought a 24k gold chain for a family wedding but later decided to sell it. However, when they approached another jeweler for selling, they were informed that the chain had impurities and wouldn’t be valued as pure 24k gold.)

Taxation benefits

When purchasing physical gold, you are liable for a 3% GST on the gold itself, along with an additional 5% GST on making charges. For sales exceeding ₹50 lakhs, a 1% TDS is applicable. Capital gains tax on short-term gains is determined by your income slab, while long-term gains are taxed at a fixed rate of 20%. In contrast, when you invest in SGBs, only the interest component is taxable, with all other aspects being exempt from tax.

Making Charges

Gold jewelry incurs substantial making charges, and when it goes out of trend, redesigning it involves additional costs. In contrast, SGBs do not have any making charges. (In 1993, my aunt had jewelry made for her wedding and later passed it on to my sister-in-law. Dissatisfied with the design, she opted to retain only the gold, necessitating significant making charges to convert it into gold biscuits, thereby affecting the overall returns on the gold.)

Liquidity

In my previous writings, I’ve emphasized the criticality of liquidity for investors. It’s essential to be able to convert paper gains into actual returns. While Sovereign Gold Bonds (SGBs) have an 8-year tenure, they offer the flexibility of early encashment after 5 years. Moreover, SGBs are tradable on exchanges, ensuring liquidity. When redeeming the bond, investors receive the prevailing market price, unlike physical gold, whose value depends on local gold vendors.

Storage

Physical gold requires storage and protection due to the risk of theft and damage. In contrast, SGBs can be held in demat form, eliminating the additional costs associated with storage.

What is the maturity and Tax structure of SGB’s?

SGBs mature in 8 years, but they can be redeemed prematurely at 5 years or extended up to 11 years. Outside these specified intervals, the RBI does not facilitate bond purchases. Therefore, it is advisable to hold SGBs in Demat form, allowing flexibility to trade them according to market conditions, especially during periods of favorable or euphorically high gold prices. Partial redemptions are possible, with a minimum requirement of redeeming 1 gram of gold.

When you redeem the bonds to RBI you don’t have to pay any capital gains tax but when you sell the bond in the secondary market i.e. the exchanges then you have to pay capital gains taxes.

Is the Gold Bonds backed by real physical gold?

Many individuals believe that SGB’s are backed by real gold but it isn’t the case. As the name suggests its Sovereign Gold bond which means it has sovereign backing or government backing and is indexed with the gold prices. So the price of the bond is decided as the 3 working day average of the closing gold prices. This money is used by the government for development projects and also for refinancing the existing debt.

Why is there a need for an instrument like SGB when we already have a Gold ETF?

Gold ETFs also provide investors with exposure to physical gold, but they are subject to taxation and do not offer the 2.5% interest available with SGBs. From a broader perspective, SGBs do not require the purchase of physical gold, thereby reducing gold imports. Additionally, the funds raised through SGBs can be utilised by the government for overall development.

- Sovereign Gold Bonds (SGBs) – A Smart Alternative to Gold Exposure - Jul 12, 2024

- Navigating the Debt Trap: Lessons from Business Failures - May 30, 2024

- Utility of Wealth in Gen Z and Their Spending Patterns - Apr 30, 2024