A cash flow statement shows the summary of cash inflows and outflows during a financial year. It gives an overall picture of the business’s liquidity. The cash flow statement consists of three different sections –

- Cash flow from operating activities

- Cash flow from investing activities

- Cash flow from financing activities

Cash flow from operating activities is one of the major sections of the cash flow statement that depicts the overall cash flow from business activities.

What is cash flow from operating activities?

Cash flow from operating activities depicts the inflow and outflow of cash into the business, which is attributable to the daily business activities. The income earned and the expenses paid during the regular course of business fall under this section. Common types of cash flow from operating activities include inflow from the sale of goods or services, salaries and wages payment, administrative and distribution expenses paid, etc.

It is paramount to note that cash flow from operating activities does not include investment-oriented revenues, purchase of assets, raising capital for the business, liability payments, etc.

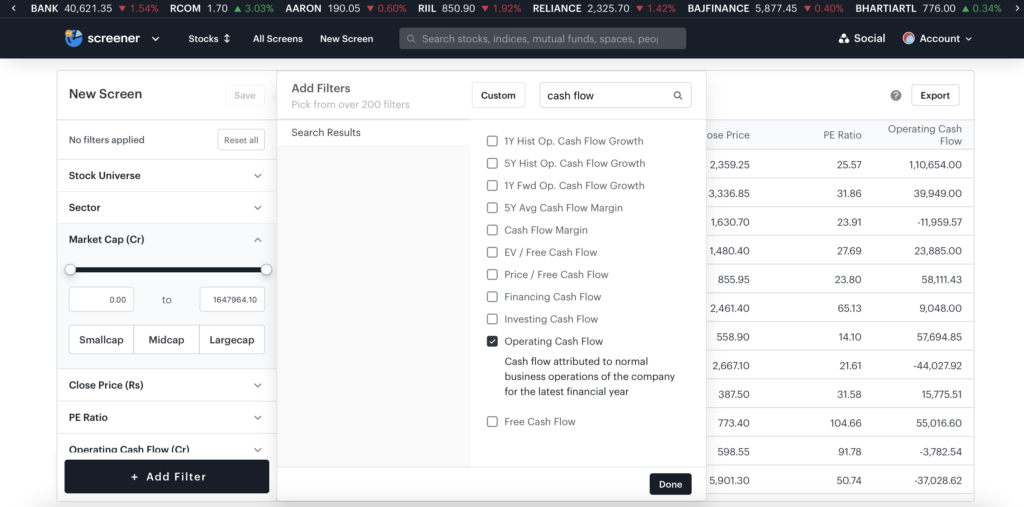

Use Tickertape Stock Screener to find the operating cash flow of a stock. You can also use other 200+ filters to find the best stock that suits your requirement.

Cash Flow from Operating Activities – Main Highlights!

- Cash flow from operating activities shows the cash inflow and outflow during the regular course of business activities.

- Common examples include sales, rent paid, salary payment, etc.

- The cash flow from operating activities can be calculated using two methods – the direct method and the indirect method.

- The cash flow from operating activities can be calculated using the formula – net income + non-cash items + changes in working capital.

- If the cash flow from operating activities is not good, a business can improve the figure by taking some corrective steps.

Cash flow statement

As mentioned earlier, the cash flow statement is a financial statement that summarises the inflow and outflow of funds. It has three main sections, aggregated to find the net cash balance at the end of the financial year. The cash flow statement can have a positive or a negative cash balance. A negative cash balance for simultaneous financial years can be a major cause of concern because it questions the liquidity of a business.

Thus, before you invest in a company, besides checking its income statement and balance sheet, a look at the cash flow statement is essential. This would give you an idea of how liquid the business is and how it generates its funds.

Tickertape Asset Pages has all the financial details you need to know about a company. Go to the ‘Financials’ tab on individual assets pages and find the ‘cash flow statement‘ of the company along with the balance sheet and income statement.

Types of cash flow from operating activities

There are two ways in which the cash flow from operating activities can be presented on the cash flow statement. These ways are as follows –

- The direct method

This is a simple way of recording the inflow and outflow of funds. Under this method, the business uses the cash basis of accounting, which means that the inflows and outflows are recorded when actual funds are received or paid out.

For instance, if the business pays the rent for office premises for the last year, the same would be recorded in the cash flow from operating activities even though the expense pertains to the last financial year. Similarly, if the business receives advance payment, the same would be recorded in the cash flow statement in the current financial year.

In other words, the inflows and outflows are recorded as incurred under the direct method. The net inflow over outflow or vice-versa forms the total cash flow from operating activities.

- The indirect method

As the name suggests, this is an indirect way to calculate cash flow from operating activities. The method starts by taking the net profit or income amount generated based on the accrual basis of accounting. This means that the income and expenses of the current year are considered in calculating the net profit. After that, a back calculation is done to generate the cash flow from operating activities.

For example, say the net profit is Rs. 1 lakh, and the business had a credit sale of Rs. 20,000. This means the net profit is inflated by Rs. 20,000 (as actual cash was not received). This amount would be deducted from the net income to get the actual cash received by the business. So, assuming that there are no other activities, the cash flow from operating activities would be Rs. 80,000 after deducting Rs. 20,000 from the net income.

Cash flow from operating activities formula

If using the indirect method, there’s a generic formula to calculate the cash flow from operating activities. The formula is as follows –

Cash flow from operating activities = Net income + Non-cash items – Change in the working capital

Alternatively, you can use the following formula too –

Cash flow from operating activities = Funds from operation + Change in the working capital

Funds from operation in this formula would mean net income plus non-cash items like depreciation, deferred tax payment, investment tax credit, etc.

How to increase cash flow from operating activities?

If the cash flow from operating activities is low or negative, the business can take corrective steps to improve the figure. Here’s how to improve cash flow from operating activities –

- If any account is overdue or a debtor is delaying payments, collect the payments at the earliest.

- Increase the turnover of the inventory. This would increase sales, which would help improve the cash flow.

- Do not prepay creditors. Pay them on time to avoid unnecessary cash outflows.

- Increase the cost of goods or services to boost the sales figure.

- Employees can be laid-off, if feasible, to cut down on salary payments.

Conclusion

Cash flow from operating activities is one of the three sections disclosed under the cash flow statement. It depicts the revenue generated from business and operating activities. Understand what is meant by cash flow from operating activities and how it is calculated. Before investing in a company, assess its cash flow from operating activities and ensure that the figure is positive so that you can invest in a profitable business.

– Meaning, Calculation, Difference With ROCE And ROI, And More")