Financial accounting is an act of recording, processing, and communicating financial data and information to stakeholders, creditors and interested third parties. It is paramount that they are accurate and well-maintained.

So, what is financial accounting? Is it the same as cost accounting? Read further to learn more about financial accounting and how it is accounted for.

You will Learn About:

What is financial accounting?

Financial accounting entails documenting, categorising, summarising, and analysing all financial transactions over a specific time period.

Financial accounting is paramount for preparing financial statements – income statements, balance sheets, cash flow statements and the statement of changes in shareholders’ equity. In a sense, financial accounting is essential to judge the financial position of an organisation and is governed by a set of local and international standards.

It is necessary to understand that financial accounting is not the same as managerial accounting or cost accounting. The major difference is that financial reporting is used for external reporting, whereas cost and management accounting is used for internal and strategic planning.

Return on equity: Highlights

- Financial accounting is a true record of all financial transactions that happen over time. It can help a company determine the true financial value of its profits and losses over a given time period.

- Financial accounting can help companies with compliance formalities and also provide data to assess the true standing of a company.

- Financial accounting also has certain drawbacks, like it is historical in nature. It records the assets at cost and does not take into account inflation or the current market value of the asset.

- Financial accounting is different from cost accounting in terms that financial accounting provides information to external parties on the company’s standing, whereas cost accounting is concerned with recording the cost of production and other internal activities.

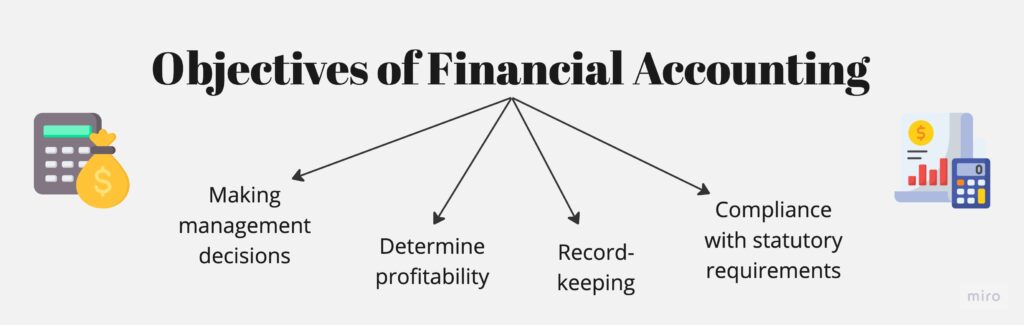

Objectives of financial accounting

Listed below are some of the few objectives of financial accounting:

- Compliance with statutory requirements

It ensures that the firm is working as per the tax rules and regulations of the Companies Act and complying with the other statutory requirements of the country in which it undertakes business.

- Record-keeping

Financial accounting helps the company to correctly identify and systematically record transactions.

- Determine profitability

Financial accounting is used in accounting for a company’s revenues and expenses, thereby helping determine profitability.

- Making management decisions

Your financial position entices the interest of stakeholders, creditors, and other parties. The accounting process enables firms and business owners to assess and evaluate financial stability and scope.

What is the main purpose of financial accounting?

The basic purpose of financial accounting is to provide stakeholders with an understanding of the true financial position and health of an organisation. Also, the data accounted for by financial accounting can be used by stakeholders for decision-making.

Additionally, through financial accounting, a company can decide its further course of action or strategize to generate greater profits.

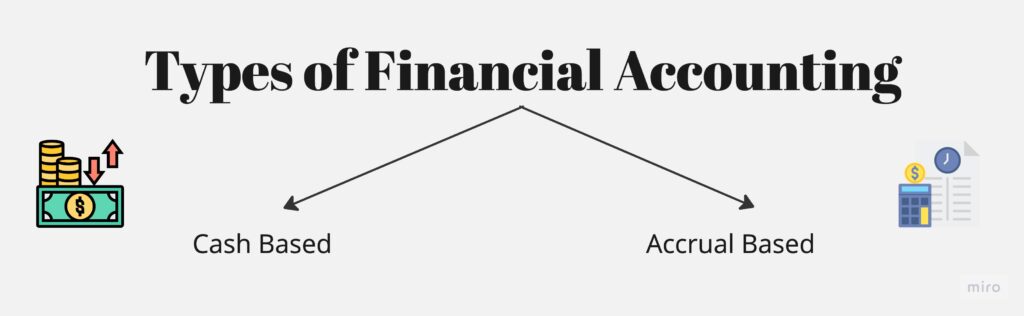

Types of financial accounting

There are two types of financial accounting, as described below. The main difference between them is the timings in which transactions are recorded.

- Cash accounting: It is used when cash transactions happen. It records a transaction when the cash is paid or received. This is an easy method which is usually used by smaller, private companies with low to no reporting requirements.

- Accrual accounting: This method of accounting records every transaction irrespective of the mode of payment. It records a transaction as they occur. Accrual accounting is usually used by large companies and is considered strict and accurate.

Types of financial statements

The 4 basic financial statements used in financial accounting are the income statement, balance sheet, cash flow statement, and statement of owner’s equity.

Balance Sheet statement

To determine if a company is worth investing in, you can look at the total assets and total liabilities of the company. This can be done with the help of a balance sheet.

The balance sheet got its name from the requirement that at any time, the total assets of a company should always be equal to the company’s liabilities, including shareholder’s equity. In case it is not balanced, it reflects some issues like incorrect or misplaced data, miscalculations, or exchange rate or inventory errors. Hence, in a balance sheet,

Assets = Liabilities + Shareholders’ Equity

You can mark a company as ‘good for further analysis’ when its assets are higher than its liabilities. But if the liabilities are higher, it is usually considered ‘not worth investing’. For a deeper analysis, various financial ratios like debt-to-equity ratio, returns on equity, etc., are used.

Profit and Loss statement

It is the profit and loss statement of a company. It is commonly referred to as the income statement, operation statement, earnings statement, or P&L statement. The income statement consists of –

- Tax and depreciation

- The revenue of the company for a certain time period (quarterly or yearly)

- The Earnings Per Share (EPS) number

- The expenses incurred to generate the revenues

The income statement gives you an insight into a company’s profitability. It helps in articulating the company’s bottom line. The P&L statement has a lot of parameters. Depending on the industry, different parameters are measured. However, there are three main parameters that can be measured for all companies to check their profitability. These are revenue, Profit Before Interest and Tax (PBIT), and net income.

For a successful company, these three factors should always be appreciated. After analysing these three factors, you can also analyse the trend in net profit for the last 5-10 yrs and operating profit to have a deeper understanding of the income statement.

Cash Flow statement

To understand the movement of money in and out of business, a cash-flow statement is used. It determines a company’s financial health and helps you analyse its liquidity. The cash-flow statement shows the net change in cash. It is usually divided into cash from operating activities, investing activities and financing activities.

To analyse a company’s cash flow statement, look for the parameter ‘Free Cash Flow’. This is indicated in positive and negative numbers, where a positive cash flow represents that the company’s assets are growing. However, a negative cash flow indicates otherwise.

Statement of change in equity

Statement of change in equity depicts the shareholding of the company. It shows the change in retained earnings, equity shares, preference shares, etc. You can check this statement in the annual report of the company.

With Tickertape, it is easy to check all the financial statements in one place. Enter the company you wish to analyse using the search bar on the Home Page. Select the stock, and click on the ‘Financial Statements’ tab. You will find income statements, balance sheets and cash flow statements there. You can view them in ‘Normal View’ and ‘Growth View’. Further, check the annual reports under the ‘Company Updates’ section of the stock pages. Explore now!

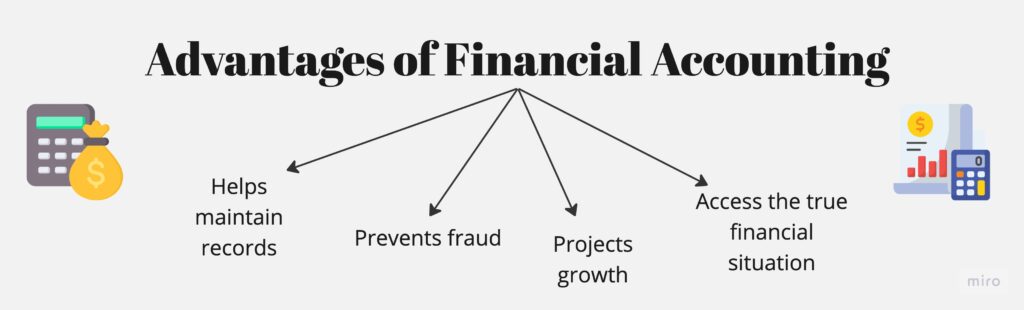

Advantages of financial accounting

The following are some of the advantages of financial accounting.

- Helps maintain records

Companies are required to keep track of all transactions made for commercial purposes. Financial accounting helps maintain proper books of accounts and systematically documents all financial transactions of the business.

- Prevents fraud

Financial accounting plays a significant role in the prevention and identification of fraud and errors. It fairly records all financial data, which is used for analysis. This data, in turn, helps decrease the possibility of fraud or inaccuracy. These records can act as evidence in a court of law in case of fraud.

- Access the true financial situation

Financial accounting provides all necessary data to owners, creditors, and stakeholders, helping them determine the true standing of the company.

- Project growth

Financial accounting provides comprehensive information on all cash flows in a firm. This can help make future growth projections.

Disadvantages of financial accounting

Below mentioned are some limitations of financial accounting:

- Only financial aspects are recorded

The fundamental problem of financial accounting is that it ignores non-financial factors such as market rivalry, economic conditions, political environment, and so on. All of these elements have a significant impact on how businesses operate.

- Provides inadequate information

Financial accounting does not provide specific information about departments, products, or other organisational activities. Separate statistics for individual activities, which may be required by management for decision-making, are not accounted for by financial accounting.

- There is no cost-cutting method

It plays no function in controlling the organisation’s costs or expenses. This is because financial accounting offers cost data after the accounting period, which means they have already been incurred. It also does not monitor for material waste, losses, or misappropriation.

- Historical cost method

Financial accounting does not take into account price variations that occur from time to time. It keeps track of the historical or real cost of asset acquisition. But an asset’s worth changes over time and does not remain constant. In this sense, financial accounting may present erroneous information.

Difference between cost accounting and financial accounting

Below mentioned are some key differences between cost accounting and financial accounting:

| Cost accounting | Financial accounting |

| Cost accounting is the branch of accounting that records the costs incurred in the production of a product. | Financial accounting is an accounting discipline concerned with recording an organisation’s financial data to show the business’s exact position. |

| Records information about the materials, labour, and overhead involved in the manufacturing process. | Keeps track of information in monetary terms. |

| Both historical and predetermined costs are considered. | Only historical cost is considered. |

| The information provided by cost accounting is exclusively used by the organisation’s internal management, which includes employees, directors, managers, supervisors, and so on. | Internal and external stakeholders, including creditors and shareholders, use the information offered by financial accounting. |

Difference between financial accounting and management accounting

Listed below are a few points which differentiate financial accounting from management accounting.

| Financial Accounting | Management Accounting |

| Financial accounting is a powerful tool for organisations. The main purpose of this method entails disclosing/publicising the company’s finances, results, and financial health of the organisation and providing valuable insights into the company’s operations. | Management accounting involves preparing and interpreting financial information for internal use by management to formulate strategies and plans for business operations. |

| The end results of this method are utilised by external entities such as shareholders, lenders, etc. | The end results of this method are used internally by managers and employees. |

| It is legally required by a company to produce financial documents and share them publicly. | Producing reports for management accounting is not legally required. |

| Financial reports have a specific format in which they must be presented. This makes it easy to compare different organisations. | Management accounting does not have a specific format. It may differ according to company or department. |

Conclusion

Financial accounting helps record, classify, and summarise financial data concerning a business. The main objective of financial accounting is to accurately prepare and record financial data to determine an organisation’s actual performance. It must be remembered that financial accounting is not the same as cost or management accounting. Understand financial accounting to access a company holistically.

– Meaning, Calculation, Difference With ROCE And ROI, And More")